Brazil’s soybean industry is experiencing a remarkable upswing — and China is at the heart of it. As global soybean prices trend downward, Brazilian exporters are seizing the moment to strengthen their position in the world’s largest soybean market. With record harvests, competitive pricing, and strong demand from Chinese buyers, Brazil has become the dominant player in global soybean trade, outpacing traditional suppliers like the United States.

This surge reflects a mix of shifting trade alliances, currency advantages, and logistical improvements that make Brazilian soybeans more attractive than ever. For traders, exporters, and analysts, these changing dynamics offer both challenges and opportunities — understanding them in real time is key to staying competitive.

Stay ahead of global trade trends with Export Genius — access verified shipment data, analyze export volumes, track pricing fluctuations, and uncover new business opportunities in the soybean market and beyond.

The numbers at a glance

- Brazil exported soybeans to China worth USD 18.9 billion in the first half of 2025.

- In 2025, Brazil’s soybean exports are projected to hit ~100+ million metric tons, up significantly from previous years.

- From January through June 2025, Brazil shipped ~64.9 million tons of soybeans, of which around 75% (~48.5 m tons) went to China.

What’s driving the surge and the price drop?

1. Record Brazilian production + plentiful supply

Brazil’s soybean harvest has been very strong. With larger acreage, improved yields, and favourable weather in key growing regions, supply has expanded. More supply globally tends to put downward pressure on prices.

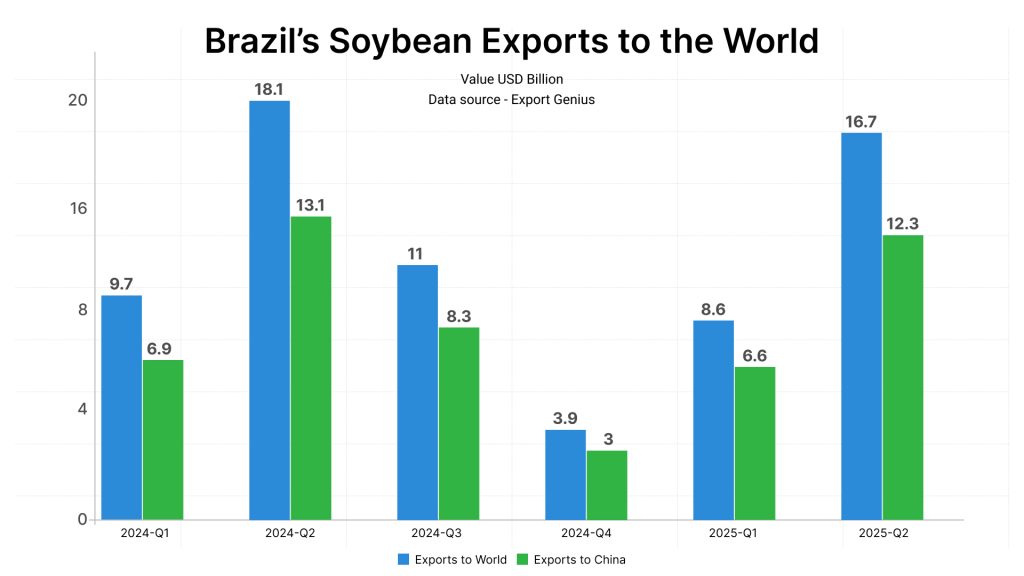

| Quarter | Exports to World | Exports to China |

| 2024-Q1 | 9.7 | 6.9 |

| 2024-Q2 | 18.1 | 13.1 |

| 2024-Q3 | 11.0 | 8.3 |

| 2024-Q4 | 3.9 | 3.0 |

| 2025-Q1 | 8.6 | 6.6 |

| 2025-Q2 | 16.7 | 12.3 |

******Value USD Billion

2. China’s pivot toward Brazil

China remains the largest importer of soybeans globally. But its sourcing has shifted markedly toward Brazil:

Brazil accounted for ~80 % of Brazil’s soybean exports going to China in recent months. In June 2025, China imported ~12.26 million tons of soybeans, ~9.73 million tons of which came from Brazil—i.e., ~80 % share for that month. This shift is influenced by trade and tariff factors (especially vis-à-vis the U.S.), as well as Brazil’s competitiveness.

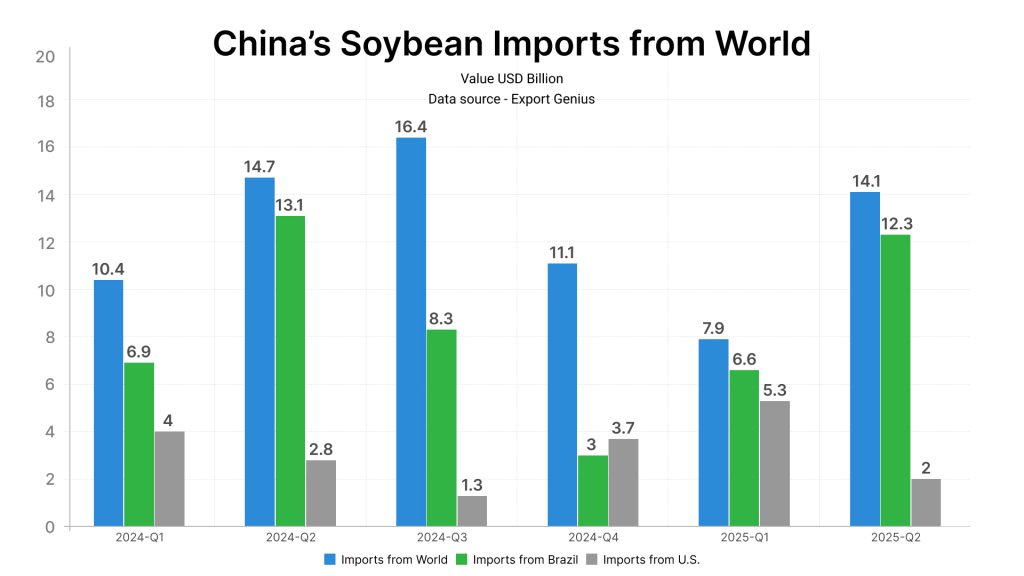

| Quarter | Imports from World | Imports from Brazil | Imports from U.S. |

| 2024-Q1 | 10.4 | 6.9 | 4.0 |

| 2024-Q2 | 14.7 | 13.1 | 2.8 |

| 2024-Q3 | 16.4 | 8.3 | 1.3 |

| 2024-Q4 | 11.1 | 3.0 | 3.7 |

| 2025-Q1 | 7.9 | 6.6 | 5.3 |

| 2025-Q2 | 14.1 | 12.3 | 2.0 |

******Value USD Billion

3. Transport/logistics & currency effects

Lower transport/landed costs from Brazilian ports, plus depreciation of the Brazilian real, have made Brazilian soybeans relatively more competitive in U.S. dollar terms. For example, export prices per metric ton in dollars have fallen.

4. U.S. competition constrained

The U.S. has lost some share in the Chinese import market of soybeans, partly due to tariffs/trade friction and partly because Brazilian supply has scaled. This gives Brazil greater leverage and market share.

Why the drop in prices matters

The combination of abundant supply + strong competition = lower prices. For many stakeholders:

Brazilian farmers/exporters may enjoy high volumes but face lower margins per ton.

Chinese importers benefit from cheaper buys (in some cases) and more diversified sourcing.

U.S. exporters are under pressure: losing market share to Brazil, especially in the key China destination.

The broader soybean/soy-meal value chain feels the ripple: feed ingredient costs, biodiesel feedstocks, etc.

Wider implications & what to watch

For Brazil

The boom in export volumes is good, but to sustain it Brazil must ensure infrastructure can keep pace (ports, rail/river logistics, crushing capacity). Also concerns about sustainability: more production, more land use change, etc (which China and global buyers increasingly care about).

For China

Having such a dominant supplier (Brazil) is efficient, but also creates dependency risks (weather shocks, logistics disruptions, crop issues). Also, buying large volumes when price falls is favourable—but could also distort domestic incentives (e.g., for soybean-meal, oilseed processing).

For U.S. and other suppliers

If Brazil continues to capture share, the U.S. will need to adjust its export strategy: maybe focus more on value-added, on different markets, or find ways to lower costs/offer unique traits.

For global markets/prices

Prices may remain under pressure for a while until some supply constraint emerges (weather, logistics, crop issues). On the flip side, if Brazil’s costs creep up (fertiliser, labour, transport), that could change the picture

Conclusion

Brazil’s surge in soybean exports to China underscores how global trade flows can rapidly realign when market conditions, production strength, and pricing advantages converge. With abundant harvests and lower export costs, Brazil has cemented its role as China’s primary soybean supplier — even as prices continue to soften.

While this trend benefits Chinese importers and reinforces Brazil’s dominance, it also exposes new dependencies and competitive pressures for other exporters, particularly the United States. As global supply chains evolve, monitoring these shifts will be crucial for traders, analysts, and policymakers aiming to anticipate future market movements.

For stakeholders across the agricultural value chain, the message is clear: adaptability and data-driven insights are essential to thrive in this changing trade landscape.

Leverage Export Genius to access real-time export data, monitor trade patterns, and uncover new opportunities in the global soybean market. Stay informed — stay competitive.